The biggest FinTech killer is time.

Teams spend months building features nobody needs yet, trying to future-proof compliance, negotiating with too many stakeholders, and end up launching late, over budget, or not at all.

The companies that win in FinTech are not the ones with the biggest teams or the longest roadmaps. They are the ones who ship fast, learn fast, and fix fast.

According to DORA’s research, the teams that ship the fastest are also the teams with the lowest failure rates, because they release in small, controlled increments instead of waiting for a massive launch.

So the question is no longer how to build more. It is how to build less, ship earlier, and stay compliant without slowing down.

Sprint-based delivery teams exist for that exact reason. Small, cross-functional teams that can design, build, test, secure, and release product increments without handovers or bureaucracy.

In this article, you will learn:

- Why overbuilding is especially dangerous in regulated finance

- How to define the smallest version of a FinTech product that can legally and safely go live

- How lean, iterative delivery lowers cost, reduces risk, and shrinks timelines

- How the right squad structure can cut time-to-market by half

- The most common traps FinTech teams fall into and how to avoid them

If you want a faster launch, a smaller burn rate, and a product that gets real user feedback instead of dying in development, keep reading.

Why FinTech Teams Overbuild (And How It Destroys Speed)

Building a FinTech product is a lot like packing for a long trip. You start with the essentials, but the moment you worry about every possible scenario, the suitcase becomes impossible to carry.

Similarly, in product development, teams don’t fail because they forgot something important. They fail because they tried to bring everything “just in case.”

Overbuilding usually starts with good intentions, but it ends with slow releases, burned budget, and a product that never reaches users. The most common reasons look like this:

- Planning for future regulation instead of current launch needs: Teams try to satisfy every possible audit before they even have real users. Instead of shipping a minimal, legally compliant core, they build for rules that may not apply for another year.

- Too many people shaping the product at once: Legal, product, security, compliance, founders, investors, and architecture; each adds “one more thing,” and the MVP quickly turns into a full-featured banking system.

- The “bank-grade from day one” mindset: Startups copy the architecture of institutions that spent 15 years evolving their stack. Instead of learning from customers, they build like they already have millions of them.

- Scaling for volume before proving adoption: Engineering puts time into containers, autoscaling, multi-region resilience, and distributed systems, even though real usage is still zero.

McKinsey’s research shows that almost two-thirds of software development effort is spent on work that never reaches the customer or fails to create value, which means speed and focus matter far more than feature volume.

Overbuilding doesn’t make a FinTech product safer or more competitive. It makes it slower, more expensive, and harder to fix.

The real advantage is building only what is required to go live, gather data, and improve fast.

The Lean MVP Model for FinTech: What ‘Minimum’ Really Means in Finance

In most industries, an MVP is the smallest version of a product users will tolerate.

In FinTech development, it is the smallest version regulators will allow.

That is the difference many teams miss. A “minimum lovable product” works for social apps and SaaS tools. A minimum compliant product is what works in finance.

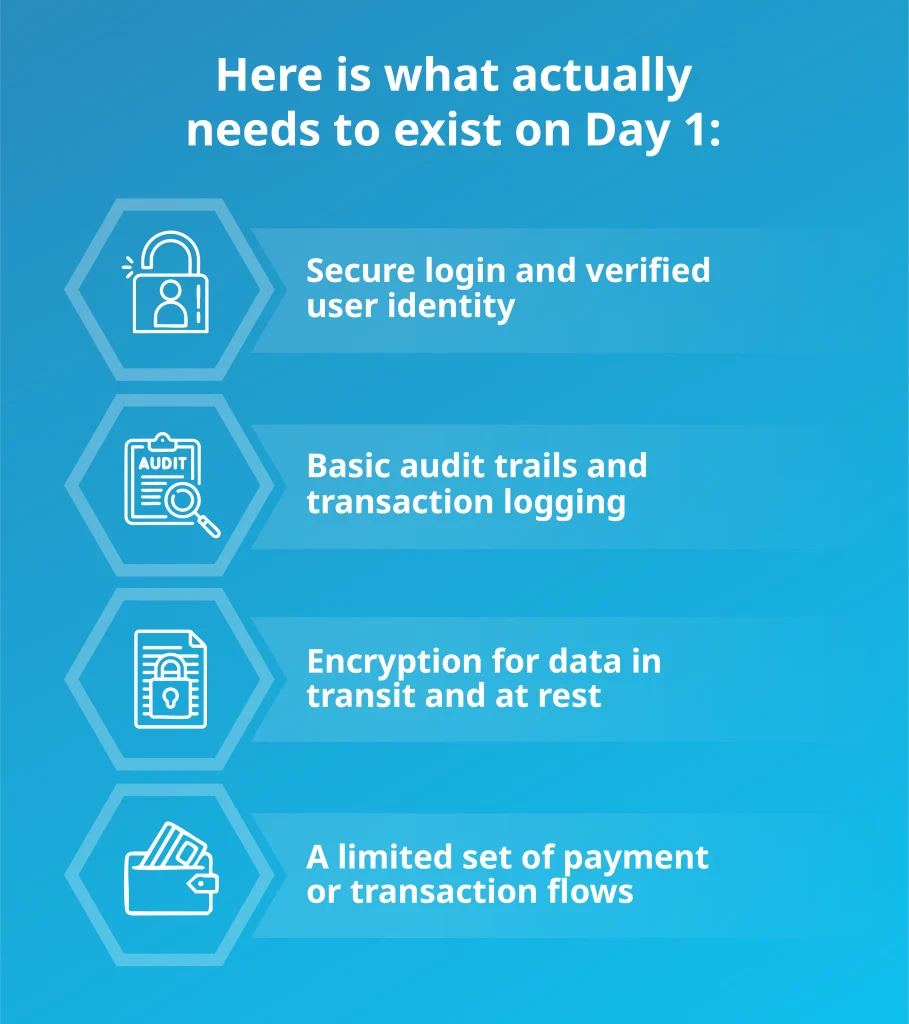

It does not need every feature the roadmap promises. It only needs the features that make the product legal, secure, and usable in a real-money environment.

A compliant MVP is not a stripped-down version of a full online banking platform. It is a focused release that proves the core value while meeting the absolute minimum regulatory and security thresholds.

Anything beyond this belongs in later iterations, not in the first release.

Real-world FinTech launches succeed because they validate one core use case under real users and real regulation, then expand.

The architecture follows the same rule. A FinTech MVP does not start with full microservices, multi-region deployments, or enterprise-grade fraud systems. It starts with modular foundations that can scale once adoption is proven.

The teams that move fastest follow one principle:

Launch the smallest compliant slice of the product, collect real feedback, and only then layer on complexity.

Build Less, Ship Faster: Lean Product Delivery Framework

If your FinTech roadmap feels slow, expensive, or overloaded, the problem is usually sequencing.

Too much gets built before anything is validated. The result is long cycles, slow feedback, and features that never get used.

Lean delivery turns product development into small, testable releases rather than a single giant launch.

Here’s how to apply lean delivery in practice:

A product that learns faster wins faster. Everything else is delay disguised as progress.

Why Small, Cross-Functional Squads Beat Large Engineering Teams

Give ten engineers a problem, and they’ll spend half the time trying to coordinate.

Give five engineers the same problem, and they’ll ship it before the bigger team finishes planning the meeting.

That’s the difference between traditional delivery and squad-based delivery in FinTech.

A squad of five to seven people can move from idea to release in a single sprint because every skill needed to ship is already inside the team: backend, frontend, DevOps, security, QA, and product.

Here’s why this model consistently outperforms traditional engineering structures:

- No handovers, no ticket ping-pong: Code, infrastructure, security, and testing live in the same team, so work flows forward instead of sideways.

- Faster decisions, faster deployments: A small group can align in minutes instead of weeks. Fewer opinions, clearer ownership, faster releases.

- Accountability improves quality: When the same squad builds and operates the product, every bug, rollback, and alert is their own. That alone drives better engineering discipline than any process document.

- The model matches what DORA calls elite performance: Small, end-to-end teams are the ones that deploy multiple times per day, recover from failures in under an hour, and keep change-failure rates below 10%; the exact metrics DORA uses to define top-tier delivery.

This is not a theory but a delivery model used by the fastest-moving FinTech products, from early-stage launches to regulated scale-ups.

Small squads go even faster when AI supports code quality, testing, and deployment analysis inside the sprint. If you want a practical view of that workflow in regulated environments, see how AI-powered engineering squads shorten release cycles without adding headcount.

The Cost Side: Lean Delivery Protects Budget and Lowers Burn Rate

FinTech products have two clocks running at the same time: the development timeline and the bank balance. The longer the first one runs, the faster the second one shrinks.

A UK study of 100 FinTech startups found that only 6% were breaking even, while 84% reported increasing losses in the last financial year, a direct result of long development cycles and late market entry.

Those numbers are about timing. The longer a product takes to reach real users, the faster the budget disappears.

That money is usually spent on things that felt “necessary” in planning, like feature bundles, dashboards, scalability work, and compliance extras, none of which have proven commercial value yet.

Lean delivery brings a big change. When a squad ships the first usable version in 8 to 12 weeks instead of 8 to 12 months, the startup keeps six to nine months of runway that would have been spent on guesswork.

Instead of burning capital on features that might never get used, the budget starts funding things that have measurable ROI:

- Real user onboarding instead of mock flows

- Real payment processing instead of demo simulations

- Real feedback from customers instead of opinions from meetings

When a founder can show investors a working product used by 50 live testers in month three instead of a slide deck in month nine, the conversation shifts. The startup no longer needs to pitch future traction because it can prove it.

That is what lean delivery really does financially:

- It turns product spend into validation spend

- It turns development cost into market data

- It turns runway into leverage instead of liability

And the FinTechs that adopt this model raise money to scale the product that already works.

Time-to-Market Advantage in FinTech: Why Speed Matters More Than Scale

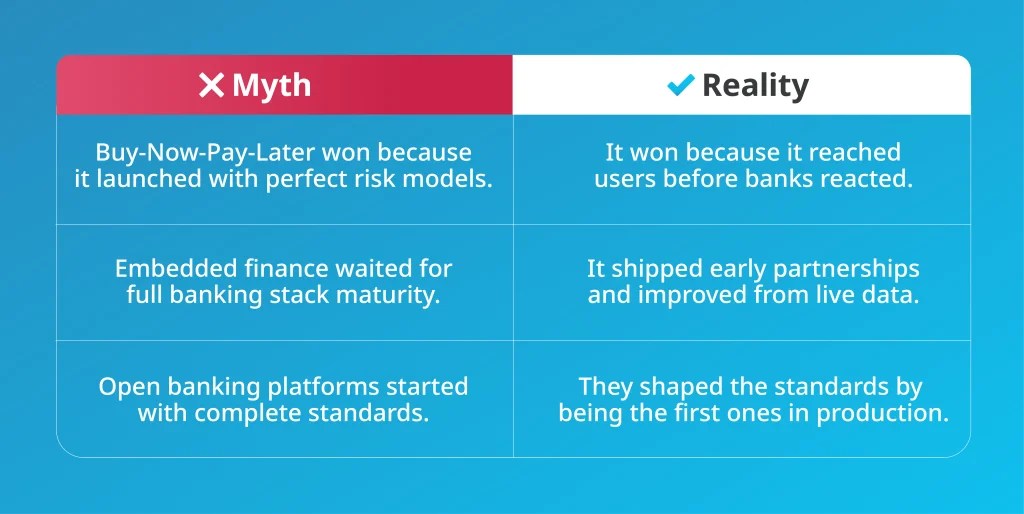

The first product to launch is not always the best, but it almost always becomes the one that sets the rules everyone else has to follow.

Speed turns an MVP into a market position. Delay turns a great idea into a late entry with higher costs, fewer users, and weaker negotiating power.

You can already see this pattern across the industry.

Open banking leaders moved quickly by choosing tools that balance speed and safety. Go is a prime example of a financial API: it handles high-throughput traffic and strict controls without slowing teams down, as shown in Go’s role in open banking.

The same principle applies to every new FinTech category: the team that ships “just enough” gains real feedback while everyone else is still discussing architecture.

Regulations shift every 6 to 12 months. Market behaviour changes even faster. A feature that took too long to build can launch already outdated, not because it was wrong, but because the world moved while it was still in development.

A fast launch does not lock you into a weak product.

It gives you an active product, one that can evolve in public, shape regulation by example, and earn customer trust while competitors are still refining documentation.

Getting to market first is about giving users, partners, and investors something real to respond to, instead of something planned.

Speed creates leverage. Scale comes later, and only for the companies that move soon enough to matter.

Lean Delivery + DevOps = Continuous Compliance

Fast delivery in FinTech only works if compliance keeps pace with development.

When every deployment is automated and traceable, DevOps turns into a built-in compliance system, not just a delivery method.

In a lean FinTech product, compliance is not something you “add later” or “prepare before launch.” It is baked into the delivery pipeline, so every commit, every deployment, and every environment is automatically checked against the rules that normally slow teams down.

Here’s what that looks like in practice:

- Compliance checks run inside the CI/CD pipeline, not in spreadsheets: PCI DSS, PSD2, encryption rules, logging requirements, all scanned automatically before code ever reaches production. If something fails, it never ships. No retroactive audit cleanup, no last-minute security rewrites.

- Infrastructure as code makes every deployment auditable: When environments are defined in code instead of screenshots or manual configuration, you can prove exactly what was deployed, when, and by whom. Auditors get evidence.

- Security shifts left instead of being patched after launch: Static analysis, dependency checks, secret scanning, and access control testing happen at build time, not after an incident. That means no freeze periods, no emergency rewrites, no “we’ll fix it in v2.”

Security is a continuous step in every build and deployment. Modern FinTech teams don’t wait until the end of a release to run penetration tests. They run automated secret scanning, dependency checks, and policy validation in the pipeline itself.

If you’re exploring how this works in practice, here’s a detailed walkthrough of DevSecOps within a CI/CD pipeline for regulated tech delivery.

Lean delivery works in regulated industries because DevOps turns compliance from a blocker into a continuous function. The product keeps shipping, the pipeline keeps verifying, and audits stop being an expensive event and become a by-product of how the team already works.

If compliance slows you down, it isn’t compliance but process debt.

Teams that keep shipping at speed also need someone accountable for the pipeline when traffic and audit scope grow. If you want a partner to run the release engine day to day, hand it to DevOps managed services and keep deployments fast, secure, and audit-ready while you scale.

All of these principles only work if the delivery engine behind them is built for speed, compliance, and continuous iteration, and that’s where most teams hit the wall.

Deployflow’s Model: Built to Ship, Not to Theorise

You need a partner that doesn’t just consult but helps you ship. Deployflow runs delivery the same way this article describes: small, sprint-based squads that build the first live, compliant version of your product in 8–12 weeks.

Each squad includes front-end and back-end engineers, solution architects, project managers, testers, and DevOps experts from day one, so there are no handovers, no external dependencies, and no delays caused by missing skills.

This model works for funded startups preparing for launch, scale-ups rebuilding slow legacy systems, and innovation teams inside online banks that need to prove a concept fast without risking compliance or reputation.

If you want a realistic estimate of how many people you need, how long your MVP would take to ship, and what the delivery cost would look like, you can run the numbers in the P-Suite squad calculator instead of guessing.

Live product beats perfect plans every time, and the teams that ship first get the conversations everyone else is still chasing.

Frequently Asked Questions About Lean Delivery in FinTech

How long does it take to build a FinTech MVP?

With a traditional delivery model, a FinTech MVP often takes 6 to 12 months because development, security, DevOps, and compliance are handled by separate teams.

With a sprint-based squad model, a compliant, working MVP can be shipped in 8 to 12 weeks because the same team builds, tests, secures, and deploys the product in continuous cycles.

The real variable isn’t “how big is the product?” but “how small can the first compliant version be?” Teams that define the smallest legal and testable version ship months faster and spend dramatically less before validation.

How do you stay compliant while moving fast in FinTech?

Compliance only slows teams down when it’s handled after development. Modern FinTech teams keep speed and compliance together by:

- Running PCI DSS / PSD2 checks automatically inside the CI/CD pipeline

- Using infrastructure as code to make every deployment version-controlled and auditable

- Shifting security reviews to the beginning of each sprint instead of the end of the project

- Treating logs, encryption, identity verification, and data handling as part of MVP scope, not “phase two”

When compliance is embedded in the delivery pipeline, fast delivery and regulatory safety stop being opposites.

What’s the difference between a prototype and an MVP in FinTech?

A prototype is a demo. It proves an idea, not a product. It may look real, but it cannot process money, store data securely, or pass an audit.

A FinTech MVP is a live, compliant product that real users can sign into, move money through, and legally operate.

The simplest way to define the difference:

- A prototype is for pitch decks.

- An MVP is for production.

If a user cannot complete a verified transaction, it is not an MVP in finance.

How do small teams handle security and audit requirements?

Small teams handle security by owning everything end-to-end.

A five-to-seven-person squad with DevOps, backend, frontend, security, and QA inside the same team has fewer handovers, fewer blind spots, and faster fixes than a 40-person org split into departments. Security becomes part of the codebase.

Audit evidence is generated automatically through:

- Automated static analysis and dependency scanning

- Git-tracked infrastructure as code

- Deployment logs stored in tamper-proof storage

- Automated test suites proving encryption, access control, and identity checks

A small, cross-functional team with the right tooling is more compliant than a large team relying on manual audit prep.

Is lean delivery only for startups, or can banks use it too?

Banks are already using it, just not everywhere yet.

Lean, squad-based delivery is now common inside innovation units, digital labs, and regulated “speed teams” inside large financial institutions.

The difference is scope:

- Startups use lean delivery to get to market before they run out of runway.

- Online banks use lean delivery to escape slow legacy processes and prove new ideas without risking the core platform.

If the product needs to move fast, reduce risk, and reach users early, lean delivery applies, whether the company has eight employees or 80,000.

Explore our BLOG

Recent articles

Modernise Legacy Public Sector Systems With Zero Service Downtime

You can replace an outdated public sector system without taking it offline for a single...

read full article

What’s Slowing Down Your CI/CD Pipeline? 5 Fixes from Real DevOps Teams

Ever tried to watch a video on slow internet? Every few seconds, the screen freezes,...

read full article

AI Engineering vs Data Science: Why CTOs Keep Getting It Wrong

Match the right discipline to the right problem, and your AI work finally ships. Confuse...

read full article